HPC Club: Supercomputing, Agentic AI & Finance with LLNL

That’s a wrap on HPC Club with Lawrence Livermore National Lab. Amazing presentation from Vanessa and Dan on Flux Framework, Agentic workflows tied in with their use in financial services.

One of the things I love most about HPC Club is its ability to enable cross domain and interdisciplinary conversations. And Vanessa and Dan exemplified this perfectly by turning their experience operating El Capitan, one of the world’s largest supercomputers, to financial services at our last event.

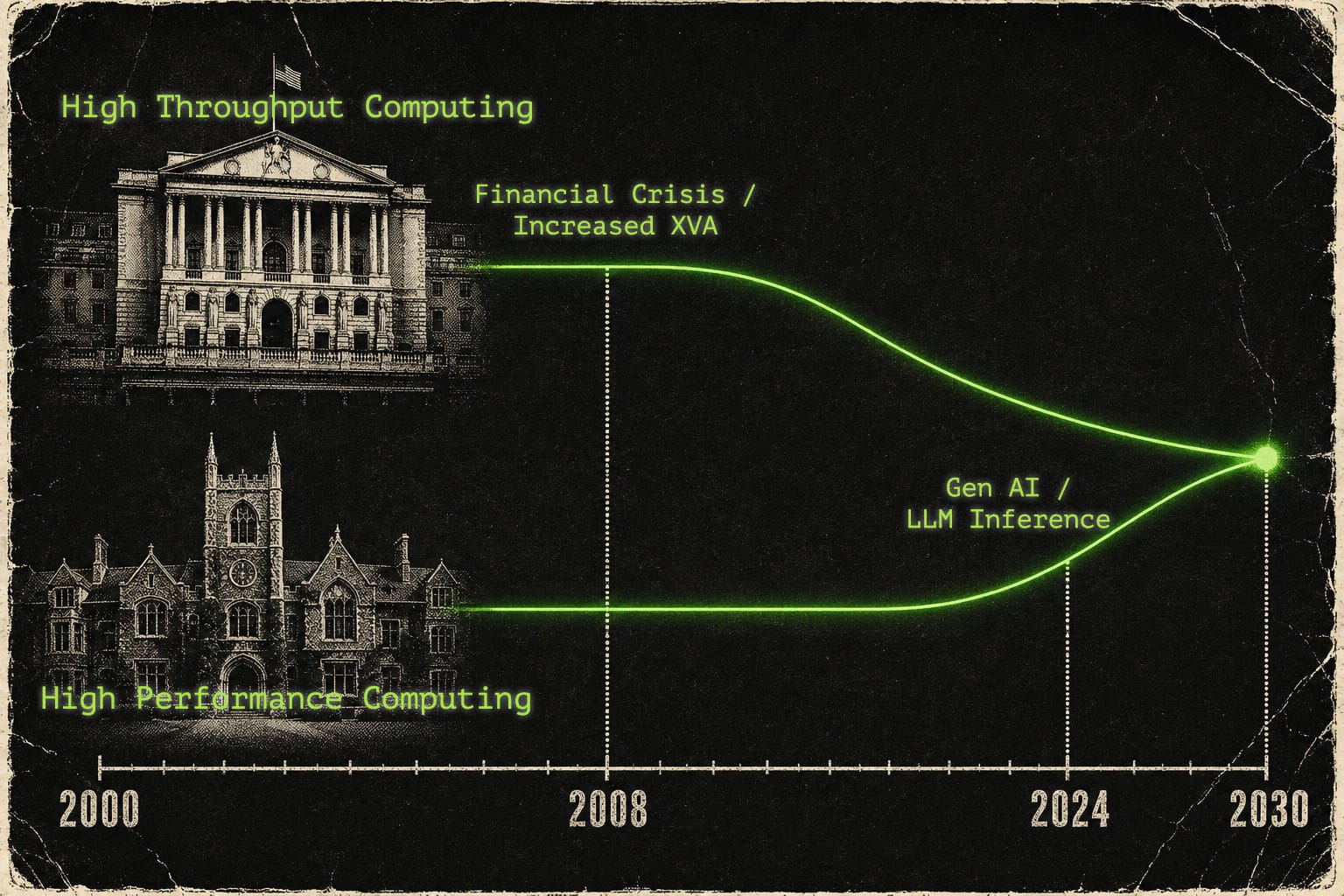

Financial services and academia have historically been seen as distinct. The very personification of high throughput computing versus classical high performance computing. But they’re converging.

And the financial services community may also be one of the last to admit it.

Most people still have the impression that financial services run only embarrassingly parallel compute (P.S: I really don’t like that term). This was true in 2000. Today the answer is far more nuanced. From 2008 or so with the increase in portfolio risk analytics a lot the demand for compute in banking has been made to fit the mould of HTC and the systems that were already available. If someone had handed the quant team a MPI manual, things would look quite different!

The arrival of LLM inference has served only to increase that pressure. Topological awareness and inter node communication are starting to become as important as high throughput rates.

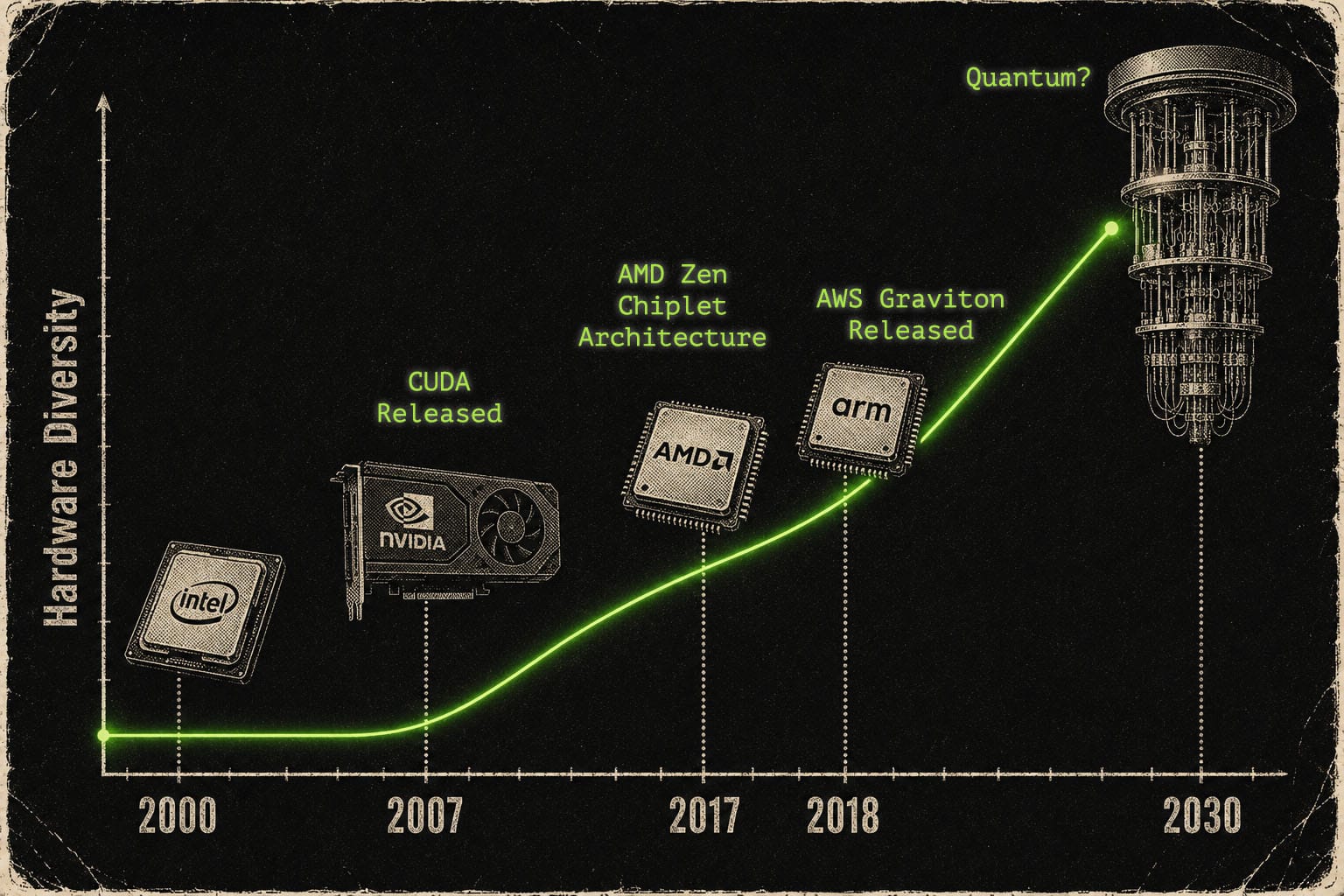

We are also operating in a world that is increasingly heterogenous. The introduction of CUDA meant dealing with CPU vs GPU compute. Although it’s been almost twenty years, honestly even this level of heterogeneity is not well solved today. Yes, it works. Yes, it can be well optimised. Not it’s not commoditised and easy to do. It should be.

Not only do we now have an increased variability in CPU architectures with the large scale adoption of ARM, RISC-V on the horizon and AMD taking centre stage from Intel in the x86 world, we are looking at an increasingly varied accelerator space. This means not only GPUs alternatives from AMD, Google’s TPU, wafer scale accelerators from Cerberas to name a few but also quantum and neuromorphic computing muscling in. These challenges are not unique to either academia or finance.

It's against this backdrop that Vanessa and Dan from Lawrence Livermore National Lab presented Flux Framework and the use of Agentic AI in HPC and supercomputing. All wrapped up with is application to a domain that new to them: Financial services.

Like I said, a perfect example of cross domain collaboration.

The full presentation is now available on YouTube. Links on the HPC Club website.